Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

One of the best things about writing this weekly markets column is that I’m creating a timestamped catalogue of meaningful events. It’s a diary of the markets. And this week, as the year 2021 came to a close, I’m looking at the major stories of the year from my columns—and they are likely to still make an imprint on 2022.

This was the first full year of the pandemic. It’s incredible that almost two years ago, I offered how to prepare your portfolio for the coronavirus outbreak on my own website. It was not yet labelled a pandemic, and the virus had yet to be called COVID-19. It shows the stock market performance during the 12 previous modern-day outbreaks since 1980, starting with the HIV/AIDS pandemic. What’s incredible about the post is that it shows how stocks reacted during the first modern pandemic and set records for performance during a viral outbreak. From the start of the pandemic in March 2020, U.S. stocks delivered more than 60%, while Canadian stocks offered a return near 40%.

Who would have thought a global pandemic would’ve been the best thing that could happen to stocks?

Inflation, we hardly know you

Inflation became a serious concern the week of January 18. Commodities were put on the table as the big, obvious inflation hedge.

In that column, we were also bullish on natural gas. Traditional oil producers were also put on the table as investment thesis. Both ideas played out in spades.

“The oil sector will benefit greatly upon successful vaccine delivery. There is incredible pent-up demand for travel by ground and air. More may hop in their cars and head back to work at their office locations. But, as we touched on last week, successful vaccine delivery is the wild card in 2021.”

Natural gas prices surged throughout 2021. The energy sector was the best performing sector in 2021.

Supply chain February blahs

I wrote about supply chain issues in early February. That risk and threat played out, contributing greatly to the ongoing and surging inflation.

“More widespread, pent-up demand for goods and services could stoke inflation. While many in the retail sector were crushed in 2020, others who are more affluent were not affected as much or at all by the pandemic. They are flush with cash as they had fewer places to spend in 2020. Spending might be unleashed.”

The continued dominance of big tech in the U.S.

If you did not own any big, OK, make that monster tech companies in the U.S., you likely underperformed the market to a great degree.

It was real earnings growth—and real revenue growth—that surprised market makers and drove the markets to new highs. Yes, U.S. stocks and U.S. big tech are expensive. But that’s where they keep the growth.

Tech has become utility-like. We depend on these companies and products to navigate our lives in almost every way.

The vaccine roll-out

It was in early March, a year after the initial shutdowns in North America, when we were first hoping for a successful vaccine rollout in the U.S.

“It appears to be a game of cat and mouse—one the markets are still trying to figure this out. A stronger economy is good, right? Well no, wait a minute, that economic growth might eventually lead to higher inflation and higher bond yields that hurt stocks. Inflation is scary and real—and lasting inflation, we hardly know ya. It’s been a while since we’ve seen real inflation. That is a U.S. link, but Canada largely will follow those trends.”

Yikes, but Jerome Powell and the U.S., The Federal Reserve got it wrong. They got it so bad. This quote is from Powell:

“We may see prices moving up, but not staying up. We see global disinflationary pressures and they are not going to go away overnight.”

Powell eventually caved on that transitory inflation theme.

Once again, oil and why it was a very good investment opportunity were given perspective in that column:

“And with greater and real economic growth comes the greater demand for oil and other commodities. That has been a constant theme mentioned and tracked in this space and, to illustrate, iShares Capped Energy Index ETF XEG is up 29% year-to-date.”

And then looking at the greater economic reopening, I wrote about how Arthur Salzer of Northland Wealth Management gave some thoughts that outperformed to a great degree.

“… value stocks should begin to perform better after posting dismal numbers since 2011. In general, value stocks such as banks have been lagging due to the negative interest rate environment globally, with North American banks doing slightly better than their European counterparts. There are also opportunities in commodities, which have likewise been weak, since the excess supplies created a decade ago, which caused mines and plants to shut down, have been used up. Gold and especially what is becoming digital gold, bitcoin, may continue to do well this decade.”

You can check the returns of those assets. Some very good calls. Gold did lag, as it has largely been replaced by “digital gold”—bitcoin.

The rise of the retail investor

Retail investors became a true force in 2021, moving the market and supporting the market. They showed up to buy the dip in the markets with regularity.

In that column Jamie Dimon, the CEO of JPMorgan Chase & Co said:

“ ‘I have little doubt that with excess savings, new stimulus savings, huge deficit spending, more QE [quantitative easing], a new potential infrastructure bill, a successful vaccine and euphoria around the end of the pandemic, the U.S. economy will likely boom,’ the JPMorgan Chase & Co. chief executive officer said Wednesday in his annual letter to shareholders. ‘This boom could easily run into 2023’.”

My favourite column of the year

The column that takes the cake for me in 2021 was the one about David Bowie making an appearance with scarcity cred, which creates value. And it can apply to bitcoin and to almost anything in the investing and collection landscape.

That week, in the same column, Eric Nutall of Ninepoint partners laid out the potential path for oil stocks.

“The explosive energy rally earlier in the year combined with recent volatility has kept much of the sidelined generalist money away from the energy space despite hugely compelling valuations. At the current oil price, the average company I model could buy back all of their outstanding shares and pay off all of their debt within about seven years with free cash flow (operating cash flow less required capital expenditures to maintain production levels). With Q1 results just around the corner and ‘modeled’ free cash flow about to become reality, I’m hopeful that ‘return of capital’ messaging will reignite interest in the sector and bring back the generalists resulting in a sector re-rating. Given severely depressed valuations, I see meaningful upside without relying on oil rallying any further (even though we see $100+WTI [West Texas Intermediate] in the years ahead).”

And certainly more fund managers are beginning to wake up to the energy reality as we moved through 2022.

I also shared this very important “inflation fighters” chart, as commodities are the most reliable defense against unexpected inflation or stagflation.

Morningstar Direct

Morningstar Direct

Sell in May? no way

In early May, I suggested why market history says don’t sell in May and go away. I’m glad investors listened.

As always, get an investment plan, invest within your risk tolerance and stick to it like glue.

In May’s last column, Canadian stocks hit an all-time high as the Canadian banks were just bursting with profits.

The rising rate environment

In late May, I took a very good look at the threat and opportunity in a rising rate environment, which is a very good host of links. And Lance Roberts of RIA Advisors offered the money post on the effect of rising rates over time.

In 2021, we also learned about the potential of a taper tantrum for stocks.

With the ongoing threat of rising rates, you might want to bookmark that column for 2022.

The beat-the-TSX portfolio

In July, I looked at the incredible beat the TSX portfolio. That stock-picking methodology has continued with a market beat in 2021. Value and big dividends are back in style.

The richest Canadian

One of the jaw-dropping Canadian success stories was Shopify. The company more than prospered during the pandemic, which propelled its founder Tobias Lütke to the podium as the richest person in Canada. Shopify is now the most valuable company in Canada, and the company helped drive the index returns in the early part of the pandemic in 2020.

Shopify had a solid year, but it did not outperform the market in 2021.

My favourite stock

In August 2021, I looked at the incredible success of Apple (AAPL) under the watch of Tim Cook:

“Investors would be happy if they bought Apple on Cook’s first day. An investment of $1,000 in Apple stock on Aug. 24, 2011, would be worth more than $16,866 as of Monday, an over 32% annual rate of return if they reinvested all dividends. The S&P 500 only returned just more than 16% annually over the same period.”

I have been a happy shareholder of Apple since early 2014. I used some of my small inheritance from my Dad (he was a teacher) to invest in Apple. Dad was a tech lover and Apple enthusiast. He would have approved. Thanks Dad.

For the week of August 27, I wrote about the Canadian banks’ impressive earnings. We also had our eye on the potential of dividend increases and buy-backs for the Canadian financials. Those dividend increase announcements eventually did arrive. And Canadian investors were overjoyed. I tallied the Canadian bank dividend increases in early December.

The dividend increases ranged from 10% to 25%.

In September, we were out of chips

The world runs on chips (semiconductors), and we were out of chips in September. I looked at the ongoing supply chain issues that were feeding inflation. Many companies still continue to have production issues and getting their products across the globe.

Semiconductors are in so many modern products. Electric vehicle production is contributing to the chip shortage. CNBC is quoted in that column:

“The shortage is thought to have been exacerbated by the move to electric vehicles. For example, a Ford Focus typically uses roughly 300 chips, whereas one of Ford’s new electric vehicles can have up to 3,000 chips.”

Earnings drive the markets higher

There was the suspicion that the stock market returns might stall as we reached peak earnings. It’s not that we didn’t have robust earnings growth for U.S. stocks, but the rate of growth was on the decline. In the end, the companies had other plans. The very robust third-quarter earnings drove stocks even higher. Canadian earnings and the markets followed suit.

Source: Seeking Alpha / U.S. Stocks – S&P 500

Source: Seeking Alpha / U.S. Stocks – S&P 500

In the above chart, you can see that stocks stalled from July and into the late fall, but those earnings were the fumes to reignite the stock market rally.

The week after, I looked at even more surprise earnings.

Inflation-fighting bonds

In November, my column included TIPS for inflation. One can certainly employ some fixed income in the inflation-fighting mix. And I wrote, we are better to look south of the border for their Treasury Inflation-Protected Securities (TIPS). There are Canadian exchange-traded fund (ETF) options offered in that article.

Looking for the double-digit stock returns hat trick

U.S. stocks are set to deliver double digit returns for the third year in a row.

The S&P 500 is up 27.5% in 2021, making it one of the best years ever for stocks. pic.twitter.com/sJZiOjj46F

— Ryan Detrick, CMT (@RyanDetrick) December 29, 2021

I call that the double-digit hat trick. That column looks at the market performance of the year after the hat trick:

“The S&P has registered a fourth straight year of positive double-digit returns four times since 1928. These include 1945 (+35.8 pct), 1952 (+18.2 pct), 1998 (+28.3 pct) and 1999 (+20.9 pct). The average: +25.8 pct.”

And just for fun, I checked out how stocks performed after the positive month in October. The momentum typically leads into positive returns for the last two months of the year. November and December are historically strong months. In that column, I cited DataTrek:

“The S&P usually rallies in November and December. Since 1980, the S&P 500 has been higher nearly three-quarters (73 pct) of the time in the last two months of the year, and up an average of +3.3 pct overall. When the S&P is higher in November and December, it’s gained an average of 5.6 pct compared to a loss of 3.1 pct during years with a negative return for those two months.”

Stocks certainly came through again with positive performance in November through to December, after a positive October.

Stock of the year: Tesla

As I wrote in this column, no stock garnered more attention than Tesla in 2021. And it’s likely that no executive inspired more headlines than Elon Musk, the CEO of electric vehicle (EV) producer Tesla.

Musk was named by Time as its Person of the Year.

Tesla and Musk moved bitcoin too, when the company began to accept the cryptocurrency for payments. He then changed his mind due to environmental concerns. He reversed course. You can buy a Tesla with green-mined bitcoin.

In 2021, Tesla was on track to increase deliveries by 80% over the previous year and it has now made roughly two-thirds of all the electric cars in the U.S. It also kicked off 2021 with its first full year of profit. At the current rate of sales, Tesla is on track to deliver more than 1 million new vehicles per year. They are also set to open mega production facilities in the U.S., Europe and Asia. It is an expensive stock, but the growth and prospects are nothing short of spectacular.

The tailwinds for Tesla and the EV industry are more like a gale force wind. The global shift to green in the attempt to reach net zero emissions targets for 2030 and 2050 might be the greatest economic force for the next decade or two.

In 2021, I initiated a position in the Amplify BATT ETF that holds Tesla and invests in the EV and battery ecosystem. I continue to add to the position. I am also building my HLIT position, an ETF from Horizons that offers exposure to lithium that is required for battery production.

Also along the greenification commodities supercycle theme, I initiated a position in VanEck’s green metals GMET ETF. This is my favourite theme for building around our core portfolios.

Of course, this is not advice. Consider these as ideas for consideration.

Omicron: Dangerous or a blessing in disguise?

At year’s end Omicron began to dominate the headlines. This variant first showed up on my columns in December, just a few weeks ago. We did not know much about Omicron in its first days, but I was hopeful that there may be a silver lining. My hope in that column was:

“If Omicron is more transmissible compared to Delta, which is the current and prevailing variant, and if Omicron causes much less death and sickness, we will move closer to the other side of the pandemic. Omicron will muscle out Delta; and theoretically, a less-dangerous variant will spread around the globe. That is wishful thinking, but it is a possibility.”

It is now the prevailing theme: Omicron will quickly bring us much closer to the end of the pandemic. We will move from the pandemic to the endemic stage. I was happy to suggest that I was ahead of Dr. Fauci on this call (wink, wink, of course).

I'm happy to have been in front of Fauci in calling the end of the pandemic. And I only have an internet degree on epidemiology. (MScInt).  #pandemic #endemic https://t.co/6AGpzd4kH7

#pandemic #endemic https://t.co/6AGpzd4kH7

— CutTheCrapInvesting (@67Dodge) December 30, 2021

Regular readers and followers of mine will know I hold an internet degree in economics.

While we might move to the other side of the pandemic in early 2022, there is certainly the risk that Omicron could inflict some serious damage among those unvaccinated and/or are in poor health. There are outbreaks in long-term care facilities and retirement homes. Let’s hope for the best on all fronts.

A new variant always presents a risk. And, as I alway say, the virus is always the wild card.

The post-pandemic period

I am hoping this is the story and dominant theme for 2022. It would be wonderful if I am able to ask: “How is your portfolio performing in our post-pandemic world?”

It seems obvious a global pandemic in the rearview mirror will open the door to continued economic growth. And that should be bullish for North American and International markets.

From this wonderful 2022 and beyond outlook piece from LPL research:

“An expanding economy is a great start, but stocks fundamentally derive their value from earnings. On the top line, the environment for companies to grow revenue next year should be excellent, with potential for above-average economic growth and some pricing power from elevated inflation. Revenue growth has historically been well correlated to nominal GDP growth, which is simply real GDP growth (the inflation-adjusted number that’s normally reported) plus inflation. Our 4% to 4.5% real GDP growth forecast for next year plus perhaps 3% inflation (about the consensus forecast for the increase in the Consumer Price Index) puts a 7% revenue increase in play.”

It is a great read and analysis, with so many relevant charts, including this chart on the recent U.S. earning history.

LPL Research

LPL Research

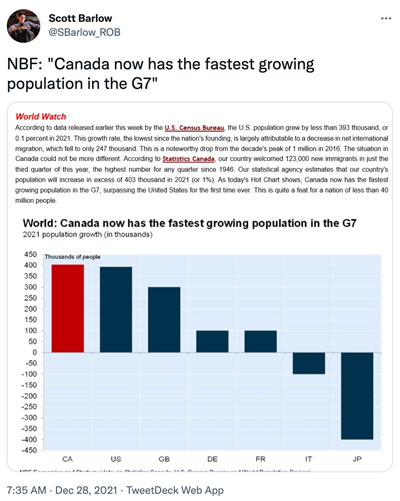

And, this is good for Canada, the most robust immigration in the G7:

Barring any black swan event, 2022 might shape up to be a solid year for investors. (A black swan is an unpredictable and catastrophic event, such as the pandemic). However, we are never free of risks. The main risk might continue to be troublesome inflation, and that could lead to the necessity of more aggressive rate hikes.

As you’ve read here, the early days and years of rate hikes cycles are not historically a threat to stocks. The recessions usually arrive three years or more later.

But past performance, and past market history, does not guarantee a repeat performance.

Let’s hope we are able to put the pandemic behind us in 2022. Hopefully Omicron is on its way out.

Here’s wishing you and your family a healthy and prosperous 2022. Thanks for reading and following “Making sense of the markets.”

Dale Roberts is a proponent of low-fee investing and he blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge for market updates and commentary, every morning.

The post Making sense of the markets: 2021 appeared first on MoneySense.

Read more: moneysense.ca

{kind=link}